Assessments - Public

Assessments

What Are Assessments

Assessments are charges that both Citizens and non-Citizens policyholders must pay in addition to their regular policy premiums when due to a major storm, series of less severe storms or other catastrophic events, additional funds are needed to pay policyholder claims.

True Cost of Insurance

Unlike a private insurance company, Citizens is required by law to levy assessments on its customers if funds to pay claims have been exhausted. For Citizens policyholders, assessments can be substantial. While Citizens remains in a solid financial position, it’s important to understand the assessment process and how it affects you.

Policyholders are impacted even if you aren’t a Citizens customer or don’t own a home. Except for the policyholder surcharge, which is paid only by Citizens’ policyholders, Citizens’ assessments can be charged on nearly every type of property and casualty policy, including but not limited to homeowners, renters, auto, boat and pet insurance policies.

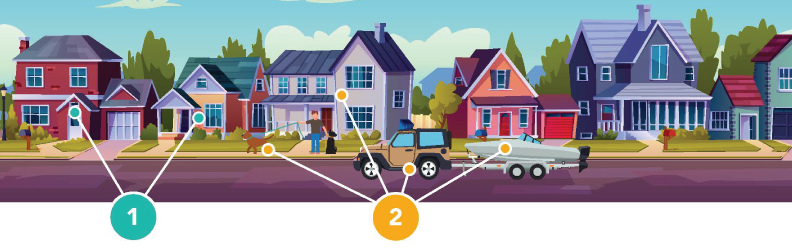

Who Pays Assessments

1. Citizens Policyholder Surcharge

Suppose a devastating storm or series of storms leaves Citizens in a deficit (meaning there is a need for additional funds to pay claims). In that scenario, Citizens is required to levy a Citizens Policyholder Surcharge of up to 15% which means policyholders could pay up to a 15% surcharge in addition to their annual premium.

Up to 15% of your premium

2. Emergency Assessment

Emergency assessments are charged if a deficit remains after the Citizens Policyholder Surcharge is applied. In this situation, Citizens must levy an emergency assessment of up to 10% per year on assessable statewide premium. This includes Citizens and private-market policyholders for as many years as necessary until the deficit is eliminated.

Up to 10% of your premium (including renters, auto, boat and pet insurance). For as long as necessary.

Surcharges and Assessments Can Add Up

For a single policy with a $3,000 premium, the Citizens Policyholder Surcharge alone could mean an additional $450 charge when you are already recovering from a catastrophic loss.

If you instead have the same policy type with a $3,000 premium from a private-market company, you will not be subject to the above $450 charge.

Cost is an essential part of your insurance decisions. See how assessments can affect the true cost of your policy following a catastrophic storm or series of storms with the True Cost Calculator.